If you’re thinking about buying a home, you’ve probably asked yourself this question at least once: Should I pay off my debt first… or move forward and buy now?

It’s a smart question. And the honest answer is: it depends.

As a mortgage loan originator, I’ve walked many clients through this exact conversation. The right decision isn’t always obvious, and it’s rarely one-size-fits-all. Let’s break it down in a simple, practical way.

Not All Debt Is Equal

First, understand this: all debt does not impact your mortgage approval the same way.

Credit cards, personal loans, and car payments typically carry higher interest rates and directly affect your monthly debt obligations. Student loans are treated differently depending on the payment structure. Some debts may have a bigger impact on your qualifying numbers than others.

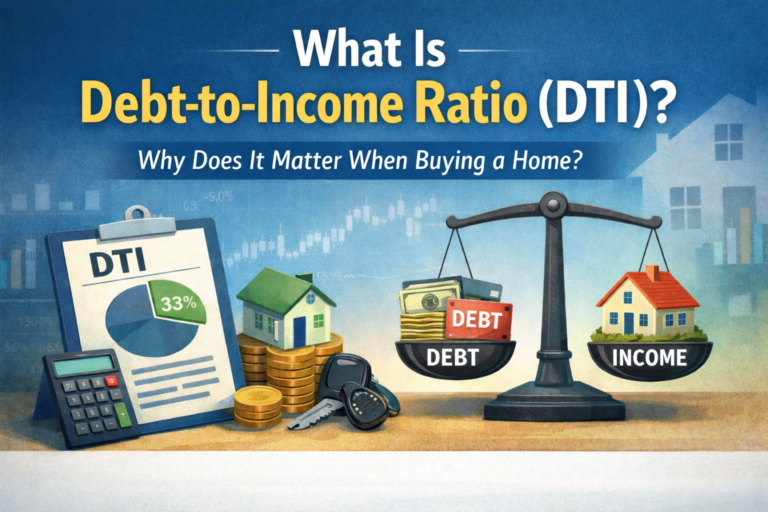

When we look at your loan application, one of the key factors is your debt-to-income ratio (DTI). That’s simply the percentage of your gross monthly income that goes toward monthly debt payments. Lowering your monthly obligations can improve this number — and sometimes make the difference between approval and denial, or between qualifying for more or less home.

But here’s the key: paying off debt doesn’t always improve your situation the way you think it will.

The Down Payment vs. Debt Payoff Dilemma

One of the biggest mistakes I see is someone draining their savings to pay off debt — and then realizing they no longer have enough funds for a down payment, closing costs, or reserves.

Cash on hand matters in mortgage lending.

In many cases, keeping funds available for your purchase can be more beneficial than aggressively paying off low-interest debt. For example, if you have a car loan at 3% interest but paying it off wipes out your down payment savings, that might not be the smartest move.

On the other hand, paying off a high-interest credit card with a large monthly payment could significantly improve your DTI and your credit score.

It’s about strategy, not emotion.

Credit Score Considerations

Another factor is your credit score. Paying down credit cards (especially below 30% of the limit) can improve your score relatively quickly. That can directly impact your interest rate and long-term payment.

However, closing accounts or making large lump-sum moves without understanding how scoring works can sometimes backfire. Timing matters.

This is why I always recommend talking with a mortgage professional before making major financial moves if you’re planning to buy in the next 3–12 months.

When Paying Off Debt Makes Sense

There are situations where paying off debt before buying is clearly beneficial:

- Your DTI is too high to qualify.

- Your credit utilization is hurting your score.

- The debt has a high interest rate.

- Eliminating the payment significantly improves your comfort level.

Homeownership should feel sustainable. If carrying certain debt will make you financially stretched or stressed, addressing it first may be the wiser path.

When It Might Make Sense to Buy Now

In other situations, moving forward with a home purchase — while still carrying manageable debt — can be reasonable:

- You have stable income.

- Your DTI falls within qualifying guidelines.

- You have sufficient funds for down payment and reserves.

- Your interest rates on existing debt are low.

- The housing market conditions support acting sooner rather than later.

Waiting to become completely debt-free can delay homeownership for years. For many people, that isn’t necessary.

The Bottom Line

The question isn’t simply, “Should I pay off debt before buying a home?”

The better question is, “How does my specific debt situation affect my ability to qualify and comfortably own a home?”

Every borrower’s profile is different. Income, credit score, type of debt, savings, loan program, and long-term goals all play a role.

If you’re thinking about buying and wondering whether to pay off debt first, I’d encourage you to have a conversation with me before making any big financial decisions. Sometimes the strategy is simple. Sometimes it requires a detailed plan.

Either way, I’m always happy to walk through the numbers with you and help you make a decision that fits your goals — not just a generic rule you read online.

If you’re considering buying a home in the next year and want clarity on your next best step, reach out. Let’s look at your situation together and build a plan that makes sense for you.