When someone applies for a mortgage, there are a handful of numbers that really matter. One of the most important is something called your debt-to-income ratio. It sounds technical at first, but once you understand it, it’s actually very straightforward. And if you’re planning to buy a home, this is a number you definitely want to know.

What Is Debt-to-Income Ratio?

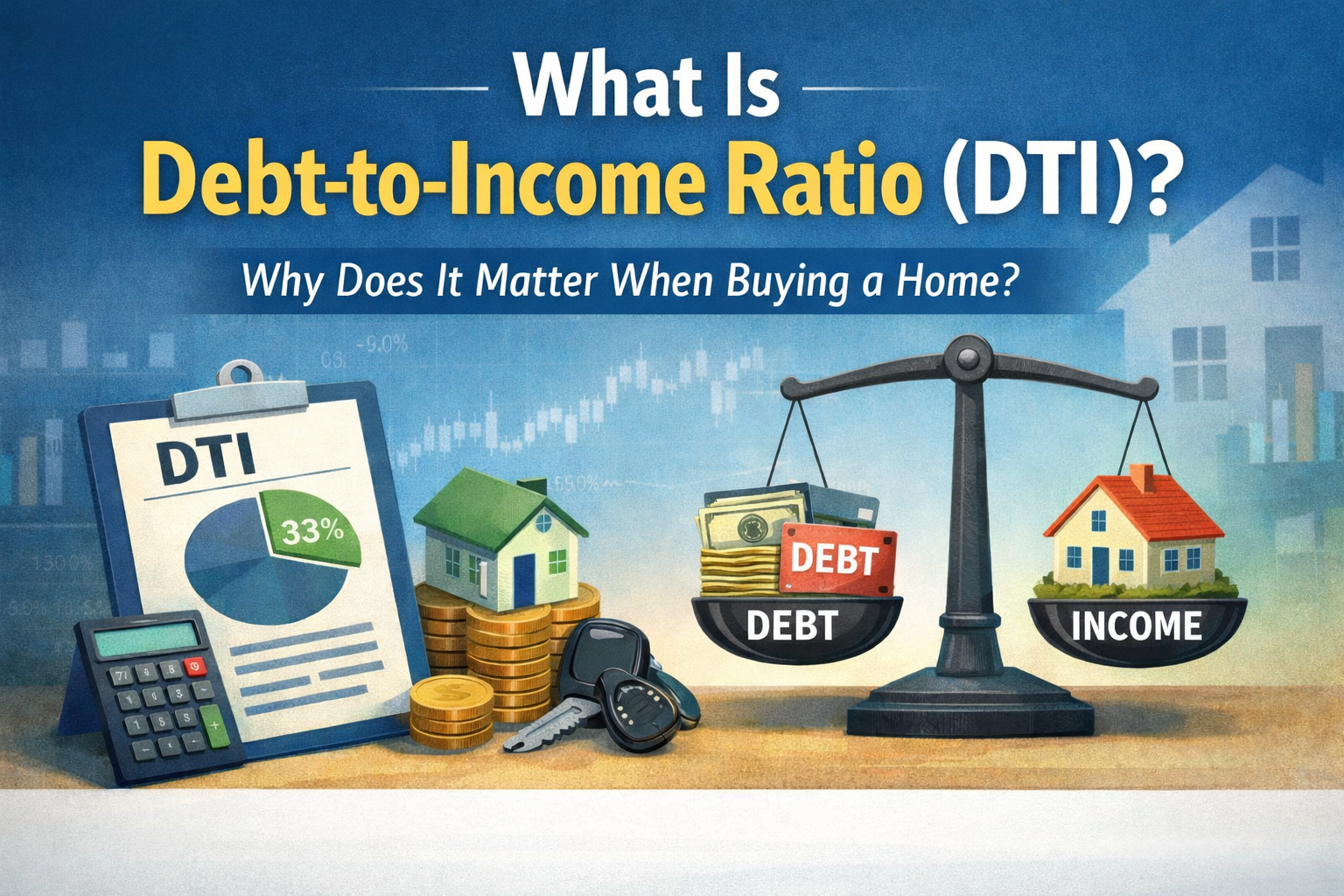

Debt-to-income ratio, often shortened to DTI, is a percentage that compares how much money you owe each month to how much money you earn before taxes. Lenders use this number to evaluate whether you can reasonably take on a new mortgage payment.

To calculate it, we add up your monthly debt obligations. This typically includes minimum credit card payments, auto loans, student loans, personal loans, and your proposed housing payment (which includes principal, interest, property taxes, homeowners insurance, and possibly HOA dues).

Then we divide that total by your gross monthly income—your income before taxes or other deductions.

For example, if your total monthly debts add up to $2,000 and your gross monthly income is $6,000, your DTI would be about 33%. That means 33% of your income is already committed to debt payments.

Why Does DTI Matter?

Lenders use DTI to measure risk and repayment ability. A lower DTI generally suggests you have more flexibility in your budget. A higher DTI can signal that your income is already heavily committed to existing obligations.

There are typically two ways this ratio is viewed.

The first is called the “front-end” ratio. This looks only at your housing payment compared to your income.

The second is the “back-end” ratio. This includes your housing payment plus all other monthly debt obligations. Most lenders focus primarily on the back-end ratio when determining approval.

Different loan programs have different maximum DTI guidelines. Some conventional loan programs may allow higher ratios if there are strong compensating factors, such as higher credit scores or significant cash reserves. Government-backed loan programs may also allow flexibility depending on the overall strength of the file.

Every borrower’s situation is unique. Automated underwriting systems also play a role in final approval decisions.

It’s also important to understand something many buyers don’t initially think about: qualifying and feeling comfortable are not always the same thing.

Just because a loan program allows a certain DTI does not automatically mean that payment will feel manageable in your day-to-day life. My goal is never just to get someone approved. It’s to help them make a wise, sustainable decision that fits their overall financial goals.

How Can You Improve Your DTI?

There are really only two ways to improve this ratio: lower your debt or increase your income.

Paying down credit cards can sometimes make a noticeable difference. Avoiding new loans or large purchases before applying is also important. On the income side, stable, documentable income increases can help strengthen your overall profile.

If you’re thinking about buying a home—even if it’s six months or a year away—reviewing your DTI early can help you plan ahead and avoid surprises later.

All loan programs are subject to borrower and property qualification. Guidelines can change, and final approval is determined based on the complete application and underwriting review.

If you’d like to know what your debt-to-income ratio looks like and how it impacts your home buying options, I’d be happy to walk through it with you. Even if you’re just in the planning stage, having a clear understanding of your numbers can make the entire process smoother and far less stressful.