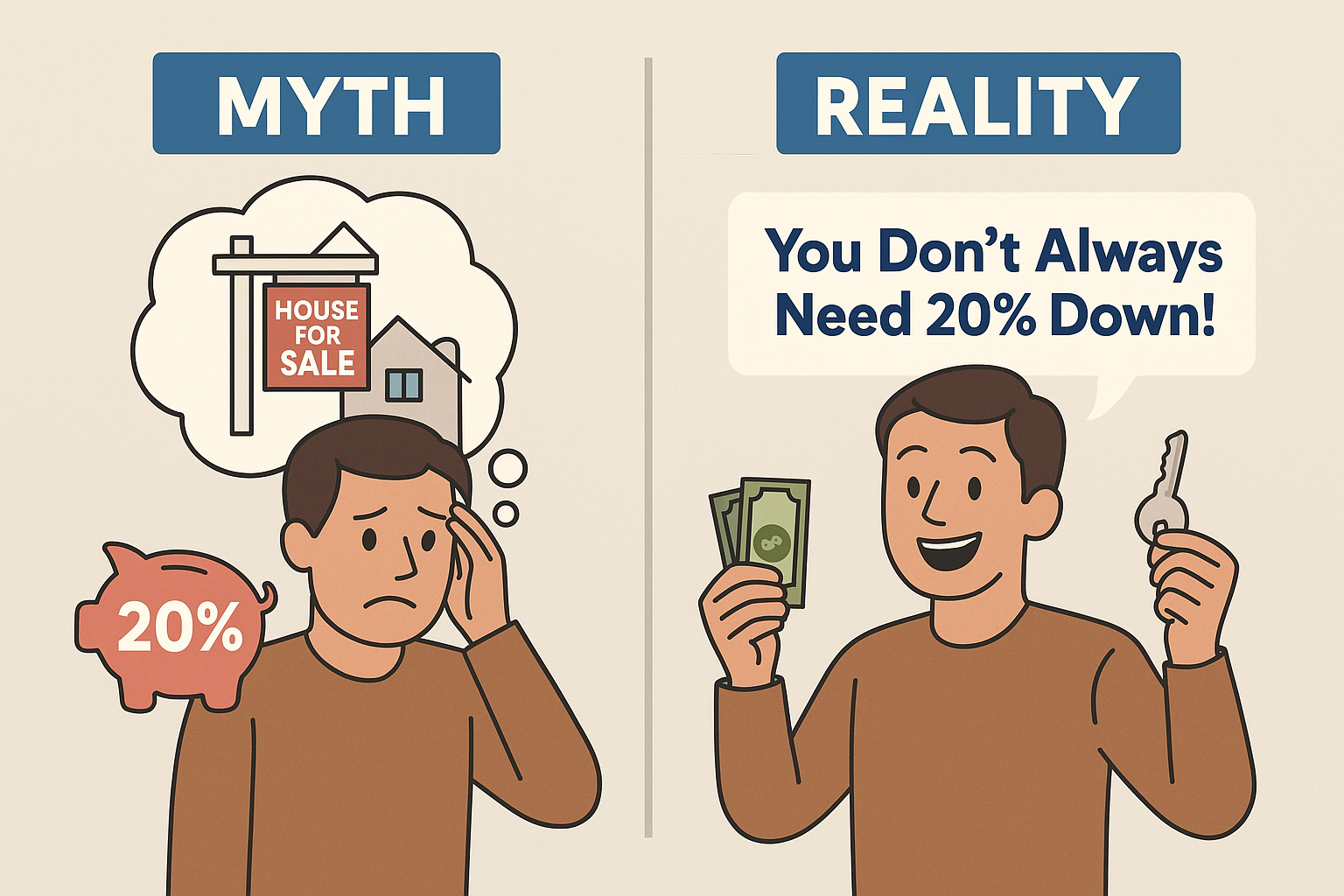

One of the most common beliefs in home buying is that you can’t purchase a home unless you’ve saved up a full 20% down payment. While putting 20% down can lower your monthly payment and help you avoid certain costs, it’s far from a requirement. In fact, most buyers today purchase their homes with much less—and in many cases, with little to no money down at all.

How Low Can a Down Payment Be?

Loan programs vary, but many allow you to buy a home with as little as 3% down. Conventional loans often offer this option to well-qualified buyers. FHA* loans require a minimum of 3.5% down, and for eligible veterans or active-duty service members, VA** loans don’t require any down payment. USDA loans also offer zero down payment options for homes in certain rural areas.

Each program has its own guidelines, including credit score requirements and limits on the home’s price or location. A licensed mortgage professional can help you determine which program works best for your budget and goals.

What About PMI?

If you put down less than 20% on a conventional loan, you’ll likely pay Private Mortgage Insurance (PMI). PMI is an additional cost added to your monthly mortgage payment. It doesn’t protect you—it protects the lender in case you stop making your loan payments.

While it’s an extra expense, PMI allows buyers to purchase a home without waiting years to save 20% down. And in most cases, PMI can be removed once you’ve built enough equity, usually when your loan balance drops to 80% of your home’s value. FHA loans have their own version of mortgage insurance, which can last longer unless you refinance into a different loan.

Why Buying Sooner Can Make Sense

Waiting until you have 20% saved might feel safer, but there’s a cost to waiting—especially if home prices or interest rates are rising. Buying sooner with a smaller down payment means you can start building equity right away. Instead of renting while trying to save for years, every mortgage payment you make helps you own a little more of your home. Over time, rising property values and your loan paydown can grow that equity even faster.

Even with the added cost of PMI, many buyers find that the equity they gain—and the ability to stop paying rent—outweigh the costs of waiting on the sidelines.

The Bottom Line

The idea that you must have 20% down to buy a home is just a myth. There are plenty of programs to help you get into a home with far less down. The key is finding the right loan and understanding how the costs fit into your long-term financial goals.

If you’re ready to explore your options, let’s talk. I’ll help you understand what programs are available and how you can start building equity in your own home, possibly much sooner than you think.

All products are not available in all states. All options are not available on all programs. All programs are subject to borrower and property qualifications. Rates, terms and conditions are subject to change without notice.

*This is an FHA program. Please call your local HUD office to verify or visit their website at https://www.hud.gov/program_offices/housing.

**This is a VA program. Current guidelines for VA Financing can be found at https://www.benefits.va.gov/homeloans/index.asp.